Requirements for Opening a Corporate Bank Account in Dubai: The 2026 Essential Guide

In 2026, securing a Dubai business account is no longer about simply having the right paperwork; it’s about proving your company has the necessary “substance.” You’ve likely heard the stories of entrepreneurs waiting up to 12 weeks for an approval only to receive a vague rejection letter without a clear explanation. We understand that meeting the requirements for opening a corporate bank account in dubai can feel like an uphill battle against shifting regulations and rigorous international anti-money laundering policies.

This essential guide cuts through the confusion to provide a clear, checklist-style path to approval. You will learn how to master the complex documentation landscape and satisfy Economic Substance Regulations (ESR) to ensure your application is processed with zero delays. We’ll preview the specific needs for both Mainland and Free Zone entities, compare traditional banks with AED 25,000 minimum balances against zero-balance digital alternatives, and explain how the 9% corporate tax rate impacts your banking profile. Our goal is to provide the expert clarity you need to secure a reliable banking partner and focus on your core business objectives.

Key Takeaways

- Master the 2026 KYC and KYB frameworks set by the Central Bank of the UAE to align your application with current regulatory standards.

- Identify the mandatory documentation and specific requirements for opening a corporate bank account in dubai to avoid common administrative rejections.

- Understand how your choice between a Mainland or Free Zone license dictates your access to traditional banking institutions versus digital platforms.

- Discover why physical presence and Ejari documentation are now critical factors in proving Economic Substance for account approval.

- Learn how a professional pre-approval check can identify red flags in your application before submission to ensure a frictionless onboarding process.

The 2026 Landscape: Why Dubai Banking Requirements Have Evolved

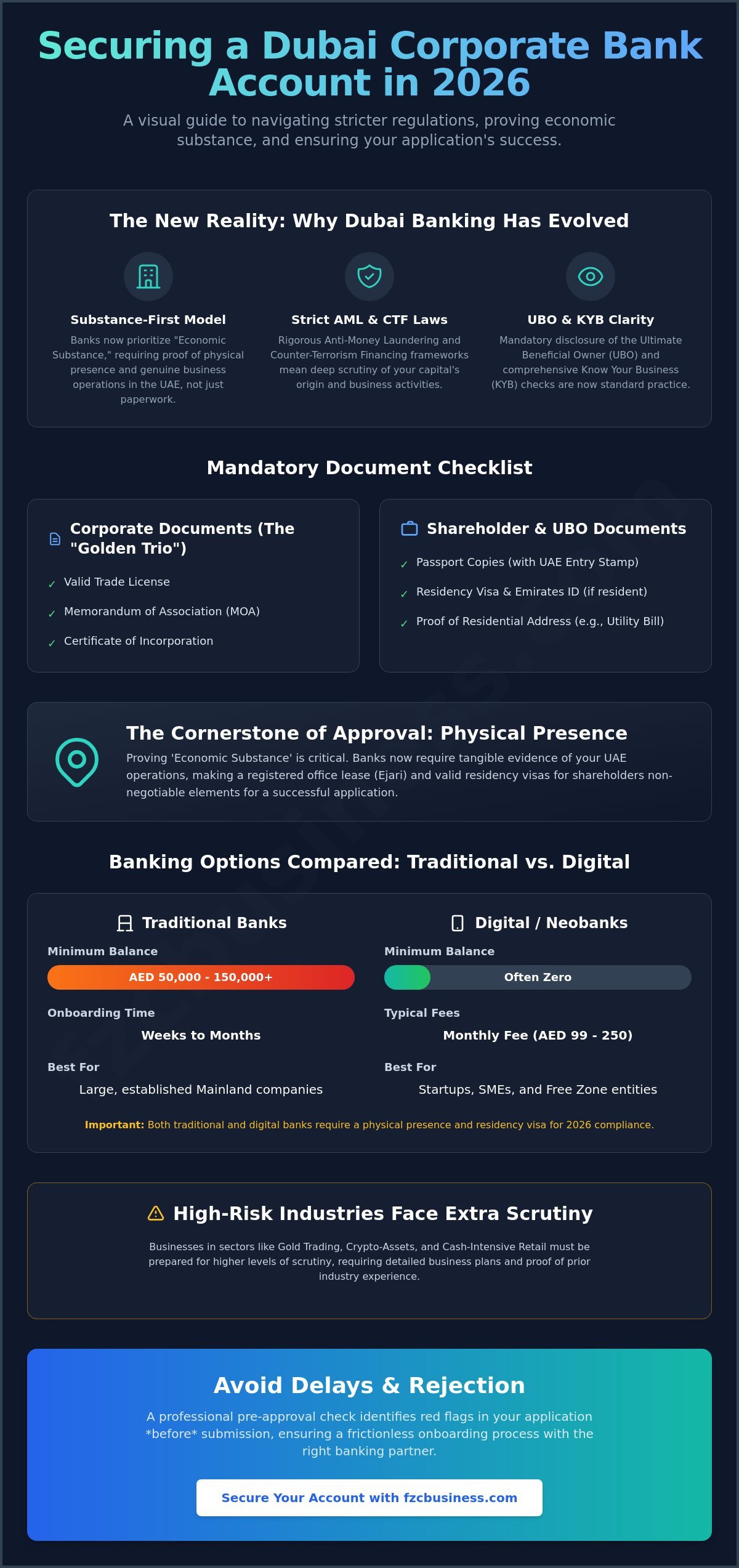

The financial environment in the Emirates has shifted toward a substance-first model. The Central Bank of the UAE now enforces strict compliance standards that prioritize international financial integrity. These 2026 requirements for opening a corporate bank account in dubai are designed to combat global financial crime, making the process more thorough than in previous years. Banks don’t just look at your balance sheet; they look at your entire corporate history.

Financial institutions now utilize advanced Know Your Customer (KYC) and Know Your Business (KYB) frameworks. These systems aren’t just about identifying who you are. They’re about understanding exactly what your business does and where every dirham originates. Transparency regarding the Ultimate Beneficial Owner (UBO) is mandatory. If your corporate structure involves multiple layers of ownership, you’ll need to peel them back to show the individual who ultimately controls the entity. This shift toward total transparency ensures the UAE remains a trusted global hub for legitimate commerce.

To better understand the current application process, watch this comprehensive walkthrough:

The Role of AML and CTF Compliance

Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) laws are the primary drivers behind the detailed questionnaires you’ll encounter. Banks must mitigate risk, which means they’ll scrutinize your source of wealth. Simply stating your income isn’t enough. You must provide bank statements, audited accounts, or sale agreements to document your capital’s origin. Certain high-risk industries, such as gold trading, crypto-assets, or cash-intensive retail, face even higher levels of scrutiny in 2026. Banks require these sectors to provide more detailed business plans and proof of previous industry experience before granting approval.

Digital vs. Traditional Banking Requirements

The rise of digital-first platforms has changed how entrepreneurs approach the requirements for opening a corporate bank account in dubai. Neobanks like Wio or Mashreq NeoBiz offer faster onboarding and often eliminate the high minimum balance requirements seen at traditional pillars. While a traditional bank might require a balance of AED 50,000 to AED 150,000, digital options often operate on a monthly fee basis ranging from AED 99 to AED 250. This makes them a popular choice for SMEs and startups.

However, don’t mistake digital for remote. Even for neobanks, the 2026 regulations require a physical presence in the UAE. You’ll still need a valid residency visa and evidence of a local address. If you’re looking for a seamless transition, Fast Zone Business can help you evaluate which banking model fits your specific industry and operational scale. We ensure your documentation is prepared to meet the specific standards of your chosen banking partner.

Mandatory Document Checklist for Corporate Accounts

Preparation is the antidote to application rejection. While the 2026 regulatory environment is strict, having a complete dossier of the specific requirements for opening a corporate bank account in dubai ensures you move to the front of the queue. The process begins with what we call the “Golden Trio” of corporate identity: your Trade License, Memorandum of Association (MOA), and Certificate of Incorporation. These documents prove your business is a legitimate legal entity recognized by the UAE Ministry of Economy & Tourism.

Banks in the UAE don’t just verify your company; they verify the people behind it. You’ll need to provide comprehensive personal identification for all shareholders and Ultimate Beneficial Owners (UBOs). This includes high-resolution passport copies with a clear UAE entry stamp or, if you’re already a resident, your Residency Visa and Emirates ID. Additionally, you must provide proof of residential address, such as a utility bill or lease agreement, for both your home country and your local UAE residence.

Corporate Legal Documents

Your MOA and Articles of Association (AOA) must clearly define the management powers and shareholding structure. If your Dubai company is owned by another corporate entity, you’ll need the full set of parent company documents. For foreign corporate shareholders, these documents must be attested by the UAE Embassy in the country of origin and the Ministry of Foreign Affairs in Dubai. It’s vital that your Trade License activity exactly matches the nature of the transactions you intend to process. A mismatch here is a frequent cause of immediate application rejection.

Shareholder and Management Documentation

Banks now require more than just ID; they want to see professional competency. You should include updated CVs for all shareholders that highlight their expertise in the chosen business activity. To satisfy “Source of Wealth” queries, you must provide 3 to 6 months of personal bank statements from your home country. This is a step many competitors overlook, yet it’s essential for proving you have the financial standing to support the new venture. If you’re unsure how to organize these personal records, Fast Zone Business can provide a pre-submission review to identify potential gaps.

The Business Profile and Financial Projections

The Business Profile is the most underrated document in your application. It acts as your company’s resume. To build a “bank-ready” profile, you must include:

- A summary of your top five suppliers and top five clients (or intended partners for startups).

- Projected annual turnover and expected transaction volumes for the first year.

- A clear description of your business model that aligns with Central Bank-approved activities.

Banks use these projections to set your account’s monitoring thresholds. Being realistic and detailed here builds the trust necessary for a smooth approval.

Mainland vs. Free Zone: How Your License Affects Requirements

Your choice of jurisdiction is the most significant factor in determining the success of your application. The 2026 regulatory framework places a premium on “substance,” and your license type tells the bank exactly how much of it you have. Mainland companies, licensed by the Department of Economy and Tourism (DET), typically face a smoother path to traditional banking. This is because a Mainland license requires a physical office and a registered Ejari, which serves as the ultimate proof of local presence. For a detailed breakdown of the licensing process, explore our guide on Business Setup in Dubai Mainland.

Free Zone entities face a more varied set of requirements for opening a corporate bank account in dubai. Banks often categorize these zones based on their regulatory history and the transparency of their registries. While Free Zones offer 100% ownership and tax benefits, the lack of a mandatory physical office for some license types can create friction. Banks are inherently cautious of businesses that operate solely through virtual desks, as these structures are harder to audit under current anti-money laundering protocols.

Mainland Banking Advantages

Mainland entities are the “gold standard” for traditional UAE banks. Because these businesses are integrated into the local economy, they often gain access to dedicated Relationship Managers who can assist with complex multi-currency needs. The physical office requirement for Mainland licenses satisfies the bank’s need for a verifiable place of business. This physical footprint allows you to open accounts with higher transaction limits and access a broader range of trade finance products that aren’t always available to Free Zone startups.

Free Zone Banking Nuances

Specific Free Zones like DMCC, Meydan, and IFZA are viewed favorably by major institutions due to their rigorous compliance standards. However, the “Flexi-Desk” challenge remains a hurdle. If your license is tied to a virtual office, traditional banks may require you to maintain a higher minimum balance, often exceeding AED 50,000, to offset the perceived risk. Specialized sectors, such as those with SHAMS or Dubai Media City licenses, may find better success with digital banks or niche departments within traditional banks that understand creative and service-based transaction patterns.

The “Offshore” hurdle has become even more pronounced in 2026. Entities registered under RAK ICC or JAFZA Offshore are now classified as high-risk by most local banks. Without local residency or a physical office, these structures struggle to meet the “economic substance” requirements. Unless you’re prepared to maintain a premium relationship balance or provide extensive proof of international trade, securing a local account for an offshore entity is increasingly difficult. If you’re currently in the planning phase, selecting a Mainland or reputable Free Zone license is the most efficient way to ensure banking success.

Proving ‘Economic Substance’ and Physical Presence

In 2026, a Dubai trade license is only the first step toward financial integration. To secure approval, you must satisfy Economic Substance Regulations (ESR). These rules ensure that companies aren’t just “shell entities” but active participants in the local economy. Banks now prioritize businesses that demonstrate their core income-generating activities happen within the UAE. This shift means that proving your physical presence is now one of the most critical requirements for opening a corporate bank account in dubai.

Compliance officers look for “Mind and Management” evidence. They want to see that strategic decisions are made locally. While it’s possible to manage a company from abroad, having a local UAE phone number and a professional email domain linked to your website provides an immediate layer of legitimacy. Avoid using generic email providers for your bank application. A dedicated corporate domain signals that you’ve invested in a permanent business infrastructure.

The Ejari Requirement

The Ejari—a government-registered tenancy contract—is often the deciding factor for account approval. For high-activity accounts involving frequent international transfers, banks almost always demand a physical office lease. This document proves you have a verifiable footprint in the city. While many startups begin with coworking space agreements, you should be aware that some traditional banks view these as higher risk. If your business model involves high transaction volumes, a private office with its own Ejari significantly improves your chances of a frictionless onboarding process. Your office location also plays a role; being situated in a recognized business district can positively influence the bank’s risk assessment of your company.

Local Operations Proof

Establishing roots in the local market involves more than just a desk. You can strengthen your application by providing a list of local suppliers, service providers, or professional partners. This demonstrates that your business is woven into the UAE’s commercial fabric. Additionally, appointing a UAE-resident director can drastically speed up the compliance check. A resident director with a valid Emirates ID allows the bank to conduct its due diligence more efficiently than it can for overseas shareholders. Always ensure that the local address on your utility bills and office lease matches the address listed on your Trade License exactly. Even minor discrepancies can trigger a manual review and lead to weeks of delays. To ensure your office setup meets current compliance standards, you can book a corporate bank account opening consultation to review your documentation before submission.

Partnering with Fast Zone Business for a Seamless Bank Opening

Choosing the right banking partner is a strategic decision that defines your company’s operational speed. While the regulatory landscape is complex, you don’t have to navigate it alone. Fast Zone Business acts as a vital bridge between ambitious entrepreneurs and the UAE’s leading financial institutions. We transform a daunting administrative hurdle into a structured, predictable process. Our team understands the evolving requirements for opening a corporate bank account in dubai and ensures your application meets the highest standards of the Central Bank from day one.

Our methodology centers on a rigorous pre-approval check. Before any documents reach a bank teller, we identify potential red flags that could trigger a rejection. We analyze your corporate structure, trade activities, and source of wealth documentation to ensure everything is “bank-ready.” By leveraging our established network of trusted bank officers at major Dubai institutions, we provide our clients with a direct line to decision-makers. This professional proximity allows us to clarify queries faster and keep your application moving through the compliance pipeline. For a deeper look at the specific banking options available, consult our Corporate Bank Account UAE Guide.

The Fast Zone Business Advantage

We provide more than just a document checklist. Our experts offer specialized support tailored to the 2026 compliance environment. We focus on the following high-value areas:

- Business Profile Drafting: We help you craft a professional narrative and financial forecast that satisfies bank scrutiny.

- Document Attestation: Our PRO team manages the complex attestation process for foreign corporate documents.

- Timeline Optimization: We aim to significantly reduce the typical 12-week wait time through proactive channel management and direct follow-ups.

Our goal is to eliminate the guesswork. We ensure that your specific requirements for opening a corporate bank account in dubai are addressed with precision, allowing you to focus on your core business objectives.

Beyond the Account: Complete Corporate Support

A corporate bank account is one piece of a larger puzzle. We offer an integrated approach by aligning your bank opening with your Trade License application. This ensures that your license activities and office setup (Ejari) are perfectly synchronized with your chosen bank’s risk appetite. Additionally, our team provides essential VAT and Corporate Tax assistance. Banks in 2026 frequently request proof of tax registration to maintain an active account status. We handle these registrations on your behalf to ensure long-term compliance and account stability.

Ready to secure your financial future in the UAE? Don’t let administrative delays hold your business back. Book your free banking consultation with Fast Zone Business today and experience a frictionless path to corporate approval.

Launch Your Dubai Venture with Financial Confidence

The 2026 banking landscape rewards those who prioritize transparency and corporate substance. By mastering the documentation checklist and choosing a jurisdiction that aligns with your operational goals, you ensure your business is positioned for long-term growth. Navigating the requirements for opening a corporate bank account in dubai doesn’t have to be a source of delay or frustration for your startup. Success is a matter of preparation and professional alignment with the Central Bank’s evolving standards.

Fast Zone Business provides the expert clarity needed to bridge the gap between your application and a successful approval. With our 100% transparency on compliance and direct partnerships with major institutions like Emirates NBD, Mashreq, and RAKBANK, we offer a streamlined path to activation. Our expert PROs, operating directly from API Tower in Dubai, are ready to manage your banking journey with precision and speed.

Secure your Dubai Corporate Bank Account with Fast Zone Business Expert Guidance. Let us handle the administrative hurdles so you can focus on building your legacy in the UAE. Your entrepreneurial journey deserves a partner that values efficiency as much as you do.

Frequently Asked Questions

How long does it take to open a corporate bank account in Dubai in 2026?

The processing time typically ranges from 4 to 12 weeks for traditional banking institutions. Digital banks offer a significantly faster alternative, often completing the onboarding process within 1 to 2 weeks. Your specific timeline depends on the complexity of your corporate structure and how quickly you can fulfill the requirements for opening a corporate bank account in dubai. Providing a complete, pre-vetted document set is the most effective way to minimize these wait times.

Can I open a Dubai business bank account without a residency visa?

No, you’ll need at least one shareholder or director with a valid UAE residency visa to open a local corporate account. Banks require a local resident to serve as a primary contact for compliance and to satisfy economic substance standards. This individual must also hold a valid Emirates ID to complete the mandatory biometric verification required by the Central Bank.

What is the minimum balance required for a corporate account in the UAE?

Traditional banks usually require a minimum average monthly balance between AED 25,000 and AED 150,000. For high-risk industries or premium corporate tiers, this requirement can reach AED 500,000 or more. Digital banking platforms provide a lower barrier to entry by offering zero-balance accounts that instead charge a monthly subscription fee, typically ranging from AED 99 to AED 250.

Why do Dubai banks reject corporate account applications?

Most rejections occur because the applicant fails to prove “economic substance,” often due to the lack of a physical office or a resident director. Banks also deny applications if the source of wealth is not clearly documented or if the business activity is on the high-risk list. Any mismatch between your trade license activities and your projected transaction volumes will also trigger an immediate rejection during the KYC process.

Do I need a physical office to open a business bank account in Dubai?

Yes, most traditional banks demand a registered Ejari tenancy contract for a physical office before they’ll approve an application. While some digital banks may accept coworking space agreements for startups, a physical office remains the gold standard for proving your business is an active local entity. This physical footprint is a core part of the requirements for opening a corporate bank account in dubai and serves as your primary proof of presence.

Can a Free Zone company open a bank account with a Mainland bank?

Yes, Free Zone entities can open accounts with Mainland banks, though they’re subject to more rigorous scrutiny regarding their operations. The bank will evaluate the specific Free Zone’s compliance reputation and your company’s local ties. Choosing a well-regulated jurisdiction like DMCC or IFZA can often make the application process smoother when dealing with traditional Mainland financial institutions.

What are the fees associated with maintaining a corporate account in Dubai?

Maintenance costs vary depending on whether you choose a traditional or digital provider. Traditional banks often charge a “fall-below” fee of AED 200 to AED 500 if you don’t maintain the minimum balance. Digital banks usually charge a flat monthly service fee between AED 99 and AED 250. You should also factor in standard costs for outward remittances, cheque book issuances, and annual KYC administrative reviews.

Is it possible to open a corporate bank account online in the UAE?

Yes, many banks now offer fully digital application portals that allow you to upload documents and complete initial screenings remotely. However, you must still be physically present in the UAE to complete the process. This involves a mandatory face-to-face meeting with a bank representative to verify your original passport and Emirates ID before the account is fully activated.